Can the trainee put down a 6 foot sub from JP Grazianos? Is one hundred chicken wings, a wing too many for one courageous man before the bell?

There probably haven’t been any eating competitions on trading floors this past week.

It’s not just HR’s fault, there’s too much information coming too fast. Investors are drinking from a firehose in whatever echo chamber they subscribe to. Whether you think we’re going back to the 70’s or the 90’s there’s confirmation bias everywhere you look.

The volume has increased. There’s more background noise, there’s more treble, and there’s way more bass. Frogs in a pot, slowly (but quickly?) heating up to boil, everyone’s screaming louder as the DJ turns up the music.

Eating competitions happen when the VIX is a teenager and bored energy manufactures entertainment. Everything’s an event in this market cycle. Same angst, different projection, and way different price action.

I always come back to the idea that markets are made up of people, so inherently this set of daily price behavior can be accurately described anthropomorphically. Mr. Market is having a moment right now. He doesn’t like his new teacher.

The drama unfolds daily, as we gyrate over every whiff of an incremental adjustment to monetary policy. Yesterday’s news is soon digested and investors have collectively recalibrated to the new narrative. But every day is a fresh opportunity to navigate the choppy waters of volatility.

It’s not always the case, there are relatively high and relatively low volatility environments. When there’s time for an eating contest, it means that not every single utterance is life or death. As the kids say, “vibing”. (Fuck. I’m old.)

There is some baseline level of volatility that becomes generally accepted by market participants within a regime. Whether this is high (2022) or low (2017), options are pricing the risk or cost of the future expected variance. While we never know what is going to come next, when Putin has boots on the ground it’s fair to assume that the price of insurance will be higher.

There are some big known unknowns in the market right now. We know there is an aggressive shift in monetary policy to fight some scary looking inflation numbers, but it’s still unclear how long it will last or what the end game will look like. While Britain just broke rank quantitative easingly, continental Europe is threatened physically on its borders and domestically with divisive elections. Crypto prices remain depressed with saber rattling (wielding?) threats of regulation and the washout of deleveraged credit.

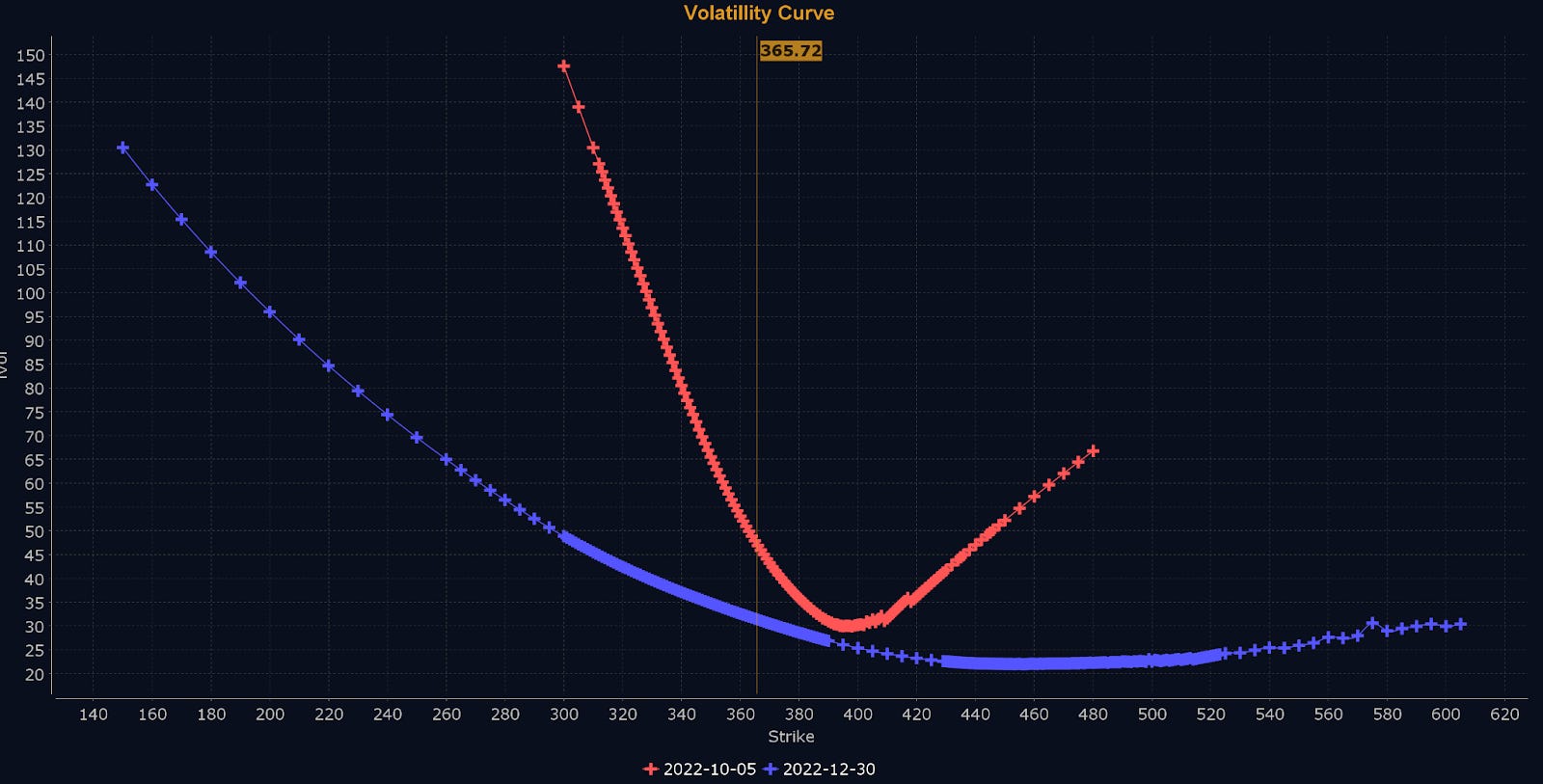

All of these factors push up the price of the at the money volatility. The whole “curve” or plot of implied volatilities shifts upward. The chart below shows the SPY options expiring next week in red, compared to those at the end of the year in blue. Next week is trading 17 points higher than December. That adds an full extra percentage point a day of expected price movement.

The other thing you’ll notice about these two curves is that the shorter dated red curve has much more pronounced wings. The skewness is steeper both on the downside and the upside. If ATM vol is pricing in the known unknowns, the skew is a measure of the unknown unknowns.

As Donald Rumsfeld said when he divided the world into three types of knowns and unknowns; “if one looks throughout the history of our country and other free countries, it is the [unknown unknowns] that tends to be the difficult ones.”

If something really unexpected happens, that’s when we have market moves that fall outside of the normal distributions. Kurtosis kicks your ass. That’s what the wings price, and why a nickel option isn’t a guaranteed sale.

In financial markets the known knowns don’t tend to be that interesting, efficient market theory has that already priced in. But there are a certain class of unknowns that we don’t know what, but we do know when. Since options are a bet on both how far and by what date, knowing when an unknown becomes known is interesting.

For events like a Fed governor speaking or an FDA announcement, we can mark our calendars, but we don’t know what the news will be or how the market will react. Depending on the magnitude of the event, we can assign some expected range of outcomes. “When Powell opens his mouth the market could go 100 points either way.”

This “event vol” is an extra dollop of variance on top of the regime scheduled background noise. Further, this event vol is elastic depending on the environment - it is larger when overall volatility is higher. News hits harder when you’re already on edge.

Markets have gotten quite efficient at pricing these known events, and adjust the implied volatility accordingly. If a “normal” day in an option’s life represents one unit of variance, and the event expects two units of variance, the further away from that event the more it falls into the background.

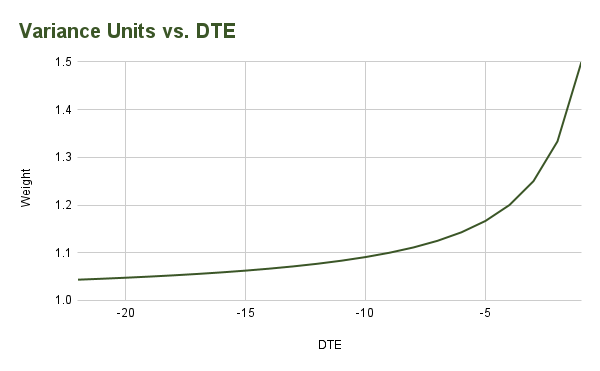

A simple model shows how the average variance units change leading up to the event, becoming geometrically more significant. When there are twenty two days left (DTE), the implied volatility of that option only needs to be 1.05 standard units per day. When there’s one day left, it’s 1.5 units per day. This is why we see kinks in the term structure of implied volatilities when there are predictable events for an underlying. In dollar pricing terms, the straddle needs to be kept constant, so IV keeps rising as time decays.

The day after the event, any remaining days in that options lifecycle get repriced at the “normal” level of one variance unit per day. This is the famous earnings crush when the news is released and the bubble of expectations deflates.

As competition seeks every incremental edge, pricing into events has gotten even more precise. For highly liquid issues there is an observable “W” shape going into a known event. This is both order flow and model driven. Customers like to buy spreads that give them positive gamma, buying the ATM options to sell the wings. Further, with a known event, the gamma on that day becomes worth more, and the ATM options have the highest gamma factor - so they should trade at a premium to their peers just before the event.

Markets don’t just evolve with respect to their pricing efficiency, there are also structural shifts in how volatility and risk are traded. Extending VIX and SPX trading into the overnight sessions distributes the trading volume across more time, but also into potentially less liquid markets. Listing additional expirations creates more tradable products, but can have recursive effects on underlying markets.

The most popular new products are 0 DTE options, introduced this past spring. The SPX index now has options expiring every day of the week for the next four weeks. While the difference between 20 and 21 days right now isn’t of major importance, the difference between 0 and 1 is all potential energy.

With a 0 DTE option, every day is an event. There are now daily opportunities to wager on where the market goes in just the next few hours - instant gratification. Pricing these is difficult. Pay too much and you watch your theta quickly bleed away. Sell too cheaply and you’ve collected pennies to lose dollars.

As you might expect, customers love these teeny portfolio WMDs. Professionals can use them to get targeted exposure relatively cheaply - the best bang for your buck greeks. Retail traders love the potential to quickly 10x their wager.

Given the macro events of this past year, it was almost a sure thing that markets would be more volatile. I don’t think on a medium or long term basis anything about the valuation mechanism is off. But on a day over day, or intraday basis, there’s an interesting argument that this new listing is creating additional volatility.

If you add liquidity to one side of the equation (options), it’s not certain there’s enough support in the other (equities, or equity futures). With the right cocktail of factors, the hedging momentum can cause the market to trip over itself in one direction. We’ve had a 2% up day and a 2% down day this week, but things look pretty close to where they were last Friday.

Part of how markets remain efficient is by digesting changes to their own structure and functioning. It’s not just the newest information about the Bank of England’s intervention that causes prices to move, the way equities move in the short term can be a reaction to the changing rules of the game.

This process will work itself out. Whether its more advanced hedging techniques from dealers or additional liquidity in the underlyings from clever arbitrageurs, markets evolve to stamp out inefficiencies. Edge is ephemeral.

The same thing will happen as we transition out of a high vol regime. It’s probably not tomorrow, but I doubt it’s a decade away. I’m not a psychologist, but from my armchair I can surmise that elevated and extended market stress is going to wear on people and that exhaustion will follow into price action.

One of my easiest hand-wavy intuitions for mean reversion in volatility is giving the following example. A VIX reading of 50 (happens about 1% of days since 1996) implies daily average moves of just under 3.5% a day. That’s 130 SPX or 400 NASDAQ points. THAT can’t possibly sustain itself.

The VIX does hit 50 when people are panicking and paying up for insurance on market moves. So far we’ve just seen a good period of sustained high volatility, and equity movements have closely tracked what the VIX is implying. A reading of 32 is exactly forecasting those 2% moves we saw this week.

Institutions are buying puts because they want protection from the bond market kicking equities down another leg. Hedge funds are buying calls because they don’t want to miss out on the relief rally that FOMOs all over itself when Powell’s third act - “The Pivot” - happens. There’s a lot of demand for vol risk premium.

Eventually a new normal settles in. The fog of Markets In Turmoil ™ lifts and volatility abates to its regularly scheduled lull of moves measured in basis points not blood. Markets are an organic system that adjust and reprice as expectations move. Staying the course through that turmoil and not getting cut up by the adjustments, is the cost of the equity risk premium.