It's The Final Countdown

Vol #116: February 9th, 2022

When the trading floors went from din to dim, we tried hard to recreate the environment.

Our offices above the American Stock Exchange were once where clerks who drew the short straw were expelled towards compliance work instead of running tickets and watching the jademasters make tea. When trading moved upstairs, things got a little bit louder at 2 Rector.

Until the geriatric senior trader demanded a library environment (he was younger than I am today), we had a pretty good time playing the soundtrack of critical market moments. Lady Gaga’s “Bad Romance” was the opening bell. Ra Ra, Ra Ra Ra. While this doesn’t sound like an obvious choice, it was originally a defiant response to HR pulling the plug on the well enunciated lyrical magic of Christopher Wallace.

The close had its own routine. When it was time to clean up your deltas around 3:30pm ET, the Wilson Phillips classic “Hold On” crooned the confidence into letting it ride one more day. And with exactly five minutes and 4 seconds to go, we launched into the Final Countdown.

Most days the close is relatively uneventful. That’s just how we liked it. Turn that up to 11. No one wants to take a trade just before the markets are about to shut for the day - who knows what could happen overnight.

Expiration was a different story, as you had to watch out for those names that were getting close to pinning around a strike. Gamma hockey sticks towards infinity as the minutes tick into the final bell. Once the closing print crosses the NYSE tape, the OCC automatically assigns or expires all your contracts, and it’s 0 or 100 delta, nothing in between.

The gamma bomb was something to be avoided. If you had a big position, it was worth paying up a few cents to close out. When there were both fewer strikes and counterparties, you could even get lucky and find someone that had the opposite position and was equally interested in taking off pin risk for fair value.

With expirations currently happening daily, these delta grenades are going off left and right. Strikes are listed every dollar in top equity names, meaning there’s always some position that’s close to pinning. While this sounds like a market maker’s nightmare, there are now plenty of traders who love it, even seek it.

I got a peek at the other side when I launched the first iteration of Harvested Financial’s offerings. In order to get clients who were new to options engaged with the concept, I set up a product called “50/50” that would find spreads that roughly offered the payout profile of an even money coin flip.

This was a good introduction to the risk management aspects of a spread. Buying a naked call is sometimes hard to value because the upside is unlimited - how much should that chance be worth? Buy-writers ask the opposite question when selling a covered call - how much premium is enough for giving away unbounded upside?

With a spread you know exactly what you can win or lose. And the only thing better than knowing that, is getting immediate feedback. Trading a LEAP means waiting years, and the serial expirations take months to come around. Weekly options meant never having to sit out longer than seven days. Combine this with increased strike listings, and you start to have a setup that allows for the construction of something close to a heads or tails opportunity.

Even with these tools, 50/50 is still an approximation because it’s not exactly possible to create a pure binary option out of the standard OCC listed contracts. When options of defined expirations and strikes settle, they have a broad range of values down to the penny, they’re not all or nothing.

In an options spread, there are three ranges to think about. Your long and short strike define these bounds. Above, below, and in between. Where the stock lands at expiration is all that matters.

If you’re long a call spread, it’s worth nothing below your long strike, the same as a put spread is worth nothing above your long strike. Both are worth the maximum at and past your short strike. That maximum value is the difference between the strikes, and your net profit is that spread minus the price you paid. Everything in between those two guard rails is a gray area.

If you bought the 140/141 call spread for $0.50, your most frequent outcomes are going to look a lot like a coin flip; many $0 and $100 marks if you keep doing that trade. But there are a hundred pennies in between where you get some partial value - neither losing or making everything.

Conceptually a binary option can be thought of as the teeniest call spread possible - no murky in between. If the distance between your long and short was small enough, you’d never have to worry about the middle.

50/50 was an interesting way to hedge or speculate on a short term event. If Apple was announcing a new iPhone this week, you might want a short term hedge against the market being disappointed by simply another megapixel on the camera.

I didn’t see a lot of that hedging flow. The most active trader by far was the one who showed up at 3pm on a Friday looking to flip a couple of hundred dollar coins. Because I’m an advisor not a broker, and this was the early days of setting up, these trades all crossed my desk for manual review. Now instead of playing whack-a-mole smashing out pin risk, I was the one running around lighting fires.

Even harder than starting those fires, was getting ready to close them out. Outside the bounds is easy - both options are worthless, or they’re both in the money and cancel each other out. It only takes a few hundred bucks in an account to buy that call spread, but having your long call exercise one hundred shares is a fourteen thousand dollar question.

While I sunset the 50/50 promotion, market wide this trading activity has continued to explode. Retail punters have something to look forward to every day. Institutions are carving out finely grained strategies to precisely manage event and greek risk. High frequency traders have also joined the fray, and with so many venues to latency arb and values ping ponging around, it’s a perfect sandbox.

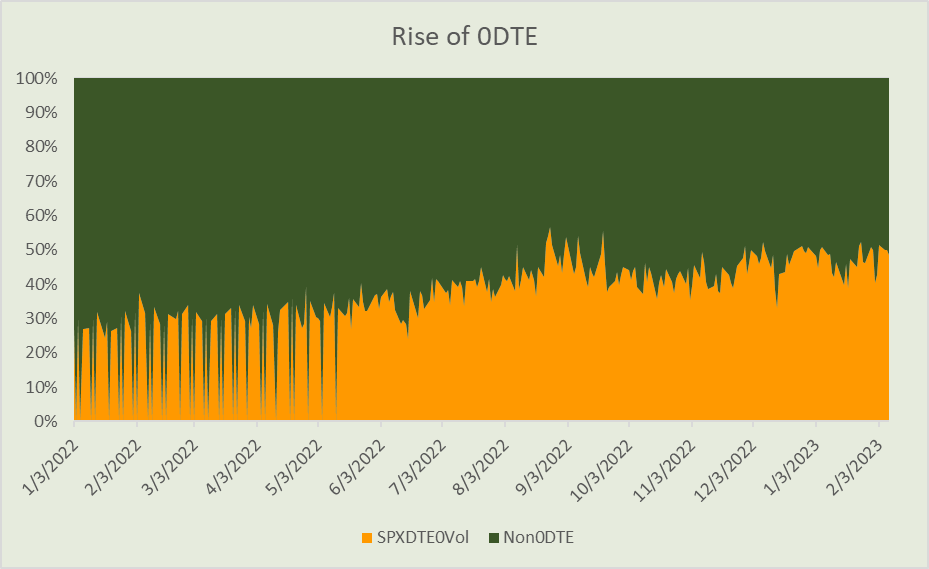

The chart below shows the continued rise of 0DTE trading. In early 2022, there days off from expiration - Tuesday and Thursdays were still fix-free then. Now there’s no respite as their percentage of SPX volume moves up and to the right.

There are days when more than 50% of SPX options volumes comes from contracts that have less than 6.5 hours on their clock. This can start to have distortive effects on how the underlying moves.

Market makers see their greek risks swing more violently when they are loaded up on short dated contracts. The smallest movements in implied volatility or even just time falling off that precipitous theta cliff will create large delta imbalances. These imbalances require a hedge, and that marginal buy or sell flow will push the underlyings around. This of course snowballs, and the market takes a drunken sailors path into the close.

For as long as I’ve been in the business there’s been a joke that hourly options are coming. It’s less of a joke every day, as we already see sports books slicing up the game into different wagers.

That’s a lot of Final Countdowns.