<Swirl><Sniff>... tell me about the decision to use 3% oak?

Understanding the process that creates a great wine is your oenophile’s fundamental research. When everyone in the neighborhood is growing the same kind of grapes in the same weather, how they tend the vines and balance the juice in the cellar is the edge that separates the best producers.

While both dimensions of production have AOC defined rules, there is broad leeway for personal touch; dosing the earth with a bull horn full of manure at the first full moon or chemically balancing pH and sugar levels once the press happens.

The resulting low intervention biodynamic pinots or ripe international cabernets show these decisions in the bottle. Better palettes can identify the subtler choices, like how choosy the pickers were in selecting grapes after a hailstorm. Or whether new or old French oak is used for maturation.

In a Zalto glass on a white table cloth, everything looks intentional. But these men and women are farmers that are scrambling to fix problems. (If you need convincing of that, go visit a wine co-op when the growing side of the house has to do their monthly tour of duty with the visitors.) Moonshine or Montrachet, the process of making heavenly elixir, has feet planted squarely in terroir firma.

The answer to the question about 3% oak can go one of two ways - thanks to Tom Hewson at the champagne blog Six Atmospheres for this framing.

A confident and self assured vintner will claim that after careful study of the growing season, a warm July produced grapes needing the spice and structure of oak. The more blunt response would be to admit there were 300L of juice left over, begging to become wine.

These are not mutually exclusive answers. Finding the best way to manage that remainder is a skill. Results come from what you plan for and how you tackle the unexpected and edge cases. Wine making, like portfolio construction, is an art that must blend both.

The efficient frontier of allocation science is cut by a fine line. Chop up your $1,000,000 account into slices of 60/40, or 70/20/10. At current prices (moving fast these days!) let’s say you can buy about 1210 shares of SPY for your equity bucket.

With $200 of cash left over. You can’t buy a full share or a bottle of Grand Cru. Fractional shares solve much of this, as do S&P 500 products with much lower price handles and unit sizes. But however you slice it, there will be some cash.

Stepping into options strategies, actual round lots get more important. It’s also preferable to trade in the most liquid products, which for indices have high handles. Any hedged equity overlay and short skew accelerant requires increments of 100 shares. Our million dollar portfolio now has 10 shares of danglers in addition to the cash.

As strategies get more nuanced, the package sizes get bigger, managing for least common denominator issues across multiple different positions. With my benchmark flavor of the AutoGULL hedged equity strategy (check out the new whitepaper!) positions are tranched across three months. If you end up with 1001 shares, we can’t evenly divide by three, so our buckets become something like 300, 300, 400, and 1.

Implementing the strategy, a nice neat idea has “unbalanced” positions. 40% of a position in one of the months instead of nice neat thirds. That month moves in time to expiration. An upside rip will hurt just a little bit more if it happens during the “wrong” window, or the downside could be better muted in a drawdown. Nothing you can plan for, just an artifact of the process. A residual that’s fairly insignificant compared to all the moving parts.

In the Backtest Notebooks, we have looked at several different flavors of the GULL implementation. My desktop folders are littered with *.csv of hundreds more. Shape that position in any reasonable way and there are real, but only relatively small differences. Yes the positions are uneven and timing matters, but not that much.

One of the ways to enhance the strategy is by managing cash efficiently. The logic goes, when the hedge pays and equities are cheap, you should buy more shares with the extra cash.

Over the last 7 years, the difference here is slight. 50bps of CAGR is nothing to sneeze at, and would pay for the tedium of someone managing this (wink wink.) It comes with more volatility because you’re going to be owning more shares, but if you squint these two pictures start to look the same.

Of course this difference matters in a technical sense, but it doesn’t matter in the “invest money to fund my goals” big picture. You can’t control the remainder, you’re better off having 1001 shares than a nice round 900 - what you do doesn’t matter.

That’s not nihilism, that’s freedom. If the remainder is only going to have a marginal impact that leaves you wide open to do something interesting, unconventional, or wildly experimental. Throw it in oak and see what happens.

One of the more romantic gestures I made to my fiancee was opening a Robinhood account. A share of WFM, RH, LULU, and of course BRK.B for an Omaha girl. Pretty quickly Don Juan was left with a remainder problem. Practically this was just my account with a goofy login, and between a few dividends and Amazon buying out Whole Foods, fast forward a decade and there was a low three figure cash balance burning a hole in my pocket.

So I bought DOGE. Mostly for the yucks, but also because Vlad makes it so easy, and just to get involved. The play portfolio is about learning, and the insignificant digits of a rounding error are the perfect place to do that. A good story, and a more suave gesture followed (a decade later) from the chicken dinner that the winner produced.

Remainders are an opportunity to try out a new trading strategy, or lean into a hunch. You’ve got extra, have fun with it. Speculative and opportunistic trades shouldn’t be any meaningful part of your portfolio (unless you’re really really good), but you can’t grow as an investor without playing with a little bit of fire.

If the demi-muid trashes your vin experimental, c’est la vie. The worst that happens with a remainder trade is it goes to 0.

Another way to think about this would be to ask the question - what does optimizing that marginal percent do for me? At what point does the asymptote get so flat that any extra effort for returns doesn’t matter?

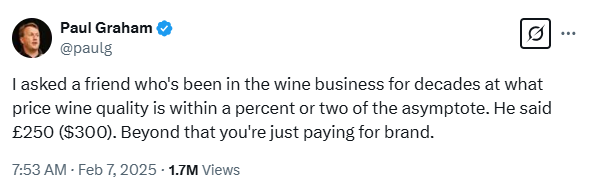

I think this sentiment is spot on. Aesthetically from a taste perspective, but also objectively from INAO designations. If we look at France, 1.4% of Burgundy wine is from Grand Cru Vineyards and 0.9% of Bordeaux production is from First and Second Growth Chateaux. The entry points for these bottles are right at that level.

If you want to taste the 1% wine, you only have to spend $300. For some of my readers that’s Tuesday night dinner (you know who you are), but just about anyone with a desire to taste something better than 99% of the competition can do so. All but the most sadistically competitive person can content themselves with that.

You’re 99% well allocated, that’s amazing. With a portfolio pushing that frontier, you’re in a very good position. The practical realities of trading in different accounts, with different stock prices, and minimum position sizes obviate perfect efficiency.

Rather than lament about why SPY doesn’t stock split so a smaller account can be more nimble, use the necessary remainder to your advantage. (Be careful what you wish for - dollar strikes on a $575 product area lot more granular.) Buy that bond put spread and discover a world where 32nds matter. Put on a crypto trade, or buy a UVIX call spread and see how hard it is to time vol.

The 99th percentile of portfolio efficiency is very accessible. There are awesome tools to do that whether you’re using options or not. But whether you couldn’t care less or are watching every tick, knowing the value (or lack thereof) of that remainder is liberating.