On the trading floor we used to talk about “process, not outcomes”. Taking a loss is part of the business, and it’s best to focus on the decision making process. In any probabilistic endeavor, no matter how weighted the coin is, sometimes it just comes up tails.

If you’re actively trading a piece of your book, the pain of being proven wrong stings. Some of the biggest winners of last year are down 50-70%. It’s perhaps more unsettling if you feel like you did “the right thing” and are still losing money.

The financial industry is well papered over with warnings and disclosures about the risk of loss and that past performance is no guarantee. But it feels better to make money. An investment is an optimistic endeavor. It’s hard to accept that if the market was up 30% last year, that there’s going to be some give back to fall in line with long term averages.

For people who would rather spend their days doing something other than staring at numbers flash or pages of 10-K filings, buying a low fee diversified index fund is about the best thing you can do. You'll outperform 80% of the professionals trying to beat you!

To be sure, there is edge in the market for active traders and investors. Whether you’re a market maker that has the built in vig from posting two sided markets and institutional flow, or a thorough analyst that has uncovered something uniquely insightful, there is money to be made beyond simple buy and hold.

But glaring facts about the underperformance of active management and the simplicity of index funds has more and more investors following the gospel of Jack Bogle, the godfather of indexing and founder of Vanguard. Most advisors (myself included) would recommend this for a big chunk of your equity allocation. It’s broadly accepted as “the right thing”.

This has led to massive amounts of capital sitting in the hands of fund managers like Blackrock, State Street, and Vanguard. Rather than a differentiated cohort of individuals with unique perspectives and objectives, there’s a certain amount of groupthink happening.

Amongst the many criticisms of this rise in passive investing is the idea that it’s anti-competitive. If I happen to own Delta, American and United Airlines stock, at any given board meeting, will I really be voting in the best interest of that specific company?

Another criticism is the impact on overall market structure. Since we like to think about extremes when we’re pricing options - what would happen if 100% of the investment community was invested in passive vehicles? There would be indiscriminate buy flow that happened every Friday payday as money gets deducted and automatically invested. There would be no individual stock pickers deciding what was good and bad, people would simply buy the index. Indexers are price inelastic - they buy at whatever the prevailing market price is. (From a dollar cost averaging perspective this can be good, but it ignores the relationship between price and value.)

Benjamin Graham said that in the short term, markets are like a voting machine, and in the long run they're like a weighing machine. For capital to be efficiently allocated to the companies that are best performing, and removed from the laggards, there needs to be someone seeking out cheap or expensive stocks. That weighing takes a bit of time.

The active managers are the ones that will be taking the other side of passive bets. The liquidity of the discretionary flows is what allows the passive indexers to lean on the work of Mr. Market. As this ratio falls, there is less and less liquidity available for passive flow, and their exposure is at an increasingly greater risk of being mispriced. It also means that it takes fewer dollars to move a market around, creating the potential for shocks.

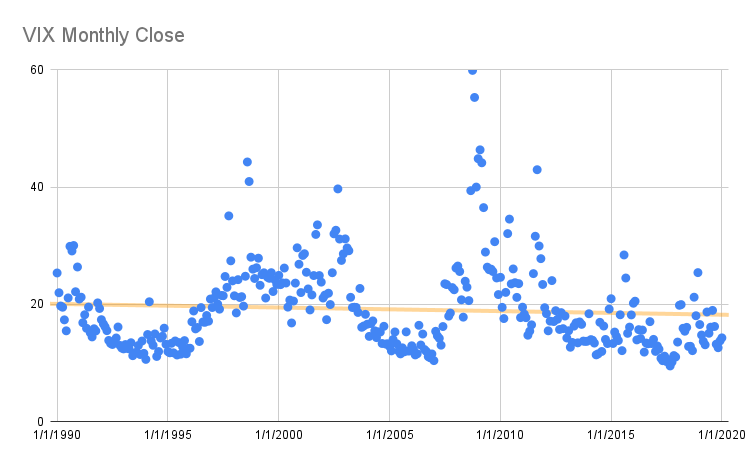

The rise of passive indexing has grown rapidly during a time when the market has continued to drift up, and on a longer horizon volatility has broadly fallen. Looking at the VIX index from 1991 through the start of 2020, we have seen a thirty year drift down, albeit with some significant spikes in between. (There could be dozens of reasons for this ranging from geopolitical, to technological, to financial.)

Things started to change once the pandemic happened. Overall VIX levels have been significantly higher the past two years. There has been a regime change where we see higher VIX readings, and some significantly larger moves, despite a trend of up and to the right. These past weeks those moves are on par with the Great Financial Crisis.

Below is a look at the daily VIX prints since the start of the pandemic, versus since 2013. 40% of the days in the last 9 years were below VIX 15, but only 2% of days in the last 2 years have been lower than 15.

What’s interesting about the VIX calculation is that it takes into account a large strip of options to come up with a single number. It’s a bit more nuanced than just the at-the-money implied volatility of the S&P500. The VIX calculation incorporates some of the skewness of the options curve. Skew is the relationship between volatilities at different price levels. If more people are buying downside protection, the ATM vol can be the same, while the VIX reads higher.

In statistics terms, these are the moments of the distribution. An options pricing skew is a probability distribution, and the forward value of the stock is the first moment or mean of the distribution. We can roughly think about the variance or implied volatility as being the second moment, and the third moment being the skew or kurtosis of the distribution.

Steeper skew may in fact be taking into account that smaller dollar amounts can now create larger pricing moves. Overall implied volatility can be lower with passive flow dominating the marketplace, but when she moves, she moves.

What does this mean for investors? Ultimately I believe that markets are efficient, and if there truly is an opportunity for active managers, they will step in and take advantage of it. From a meta perspective though, timing active management versus passive investing is another form of market timing, and something individuals aren’t particularly good at.

On the long road to financial success, the bumps in the road are inevitable. Market regimes change, and the bumps are relatively bigger and smaller. Unfortunately knowing about them in advance doesn’t necessarily make them sting any less.