Tips forward, risk on

Vol #216: February 27th, 2025

Tips forward.

There are many ways to carry your skis, but only one shows you’re ready to drop in. Keep your shoulder between the bindings, with the tails high enough to clear passerby.

Tradition runs strong amongst those willing to strap themselves to waxed rocket planks and slide down ice faces. My favorite mountains to visit combine the potential for journal notching runs with a deep sense of place. Zermatt. Alta. Stowe.

Most of the terrain in the US opened less than a hundred years ago. Steamboat, Mt. Hood, and Taho were developed in the 1920s, and the early trails at Stowe were cut by the Civilian Conservation Corps during the Great Depression. A bit of Austrian sparkle and old world credibility arrived with the Von Trapp family installing themselves in the 1940s.

Compared to when I first skied it as a teenager, things have changed. Most notably, my ability to tackle the Front Four. Considered some of New England’s toughest terrain, the fiercest of the double diamonds is Goat. Named long before Muhammad Ali’s nickname cemented into a 1990s hip hop and eventually sports acronym, the trail is known for wrenching corkscrews and general ornery-ness. It bends north away from the lift line, and narrows quickly into a single chute. There are no outs, here you’re committed.

Sorry to disappoint, but no spectacular wipe outs from me, barely a skid. Yet despite an improvement in technique, I wasn’t pounding off the bumps as hard as I used to. My risk preference has changed. So have my knees.

Individual lifecycles keep turning. The need for speed seems to have been genetically transferred to the next in line. I’m not exactly loading up on treasuries here, but my approach to the mountain’s potential has shifted.

Stowe itself has also changed significantly in the past two decades. While it’d be easy to blame Vail Mountain Resorts for bringing the corporate state outdoors, the truth is long before their $41M acquisition in 2017 the place was run by AIG. Insurance magnate Cornelius Vander Starr was frustrated with the wait back in 1943 and decided to finance a second chair, later divesting his personal acquisition to the company he founded. His name still graces the second most technical of the Front Four.

Every ski resort has their own culture. Head over to Europe and lifts open late, mostly to get everyone to their coffee and cigarette at the top of the mountain before the club opens at noon. But what used to be a cozy lodge for Green Mountain woodchucks, now has $2k/sqft condos, fire pit cabanas circling the ice rink, and a Whistle Pig tavern. WTF!

While your preferences as a consumer, user, and trader might change, the underlying market and marketplace will be shifting too. Strong winds closing lifts are the circuit breaker you can’t control - liability management clearly runs deep in the Stowe culture. More families coming over Presidents Day week means the grooming cats widen their coverage. And in 2025 there’s more demand for fresh tacos from a celebrity chef than the nostalgia of overcooked burgers in a hut.

If you want the experience of knee pounding volatility, you’re gonna have to hike to a different market. Things change, you change, shit happens. Whether it's just the decay of theta or a serendipitous (calamitous) change in your life, every investor is different from who they were yesterday or last year. And because the market’s participants are constantly changing, so are the resulting opportunities and their relative prices.

Returns are a function of price, not strategy. This means with everything other than buy and hold, any robust strategy has to take current market price into account. “Selling covered calls” doesn’t produce alpha, collecting more premium than realized volatility manifests does. Fixed opportunity capture won’t adapt as market conditions change, and is highly unlikely to have persistent outperformance over different market regimes.

A few weeks back, the inimitable @bennpeifert posted the below chart. A nice long 27 year backtest showing the benefits of selling 10% OTM index calls. A quick look and I can already hear the terminals firing up to slam bids.

The point to make here though is not that covered calls are a panacea, but that the chart presentation belies a significant shift in performance. With a linear Y axis, it’s difficult to tell that all of the outperformance of this strategy happened pre-GFC, and that since 2012 the SPX has outperformed +330% vs. 263%.

Calls were a good sale - an overcompensated risk. But eventually everyone realized it, so now they’re not. The markets have gotten significantly more efficient at pricing the volatility risk premium. That comes hand in hand with tighter markets and cheaper, faster execution. A mispricing stamped out is an opportunity to trade better priced options in other risk transfer strategies.

If you’re looking to sell overpriced risk, time to move on. Thanks to public markets, decentralized protocols, and other “exchanges”, there’s a Polymarket bet on a college student’s relationship status, a DraftKings line on points scored in the third quarter, and the Robinhood app to yolo some DOGE ahead of Elon’s next antic.

There’s a massive bubble in accessibility. The market risk preference feels like it’s making a secular shift. The ability to risk money is everywhere. But what about MY money. It’s hard to know if that means a bubble in prices or not.

The critiques of growing financial nihilism and the risks of the persistent passive bid in equity markets are not unfounded. Securitization and trade-a-bet-ability of just about everything creates a different culture of risk. One that believes that double or tripling overnight only lands you on the lesser moons. “This project’s an easy 5x at TGE bro.”

We hear of the wilting dominance of 60/40 as an investing model. Ever prone to the most recent history, anyone who first started buying stock in the last two decades will see this as an underperformer to equities, and even worse a failed hedge during the 2022 bear market. Portfolios now tilt towards pure stock, and are spiced with diversifiers like crypto or leveraged ETFs that do more to amplify than mute risk.

Only the future knows whether this risk culture will be rewarded or when and if a snag is inevitable. Assessing the market’s risk preference is far harder than understanding your own. Which isn’t so simple in the first place. Further, you have no control over the outcomes. If you’re flush with liquidity and the market is overpriced, you’ll simply have to be patient to see returns.

I have no idea what’s coming next. Nobody does. The only thing you can do is make sure you’re ready for whatever it might be. If you’re going to be picky about the when and the how of your gains over the long term, it’s going to cost you absolute returns.

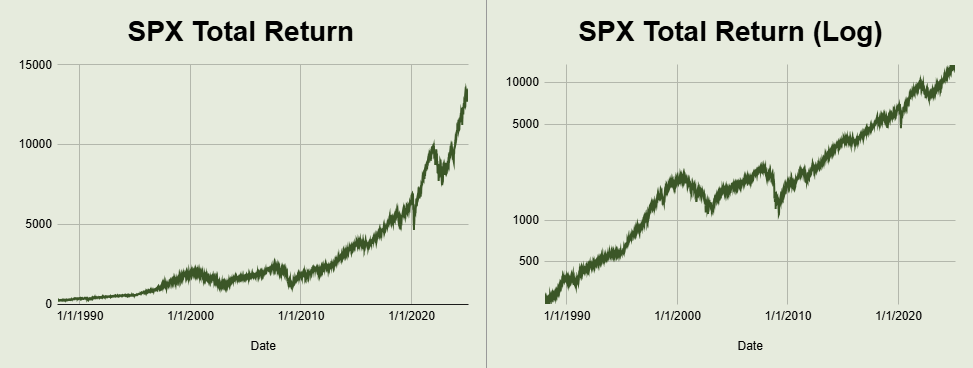

One solution to better presenting the chart above would be to use a log return. When done below, it turns the SPX from looking like a ticker about to meet its maker to something with relatively consistent return and volatility characteristics.

If we look at the SPX returns by calendar year, it might also feel like we’re “due”. The SPX went up 1000 points in the last year. Not only do you have to think in percentage or log terms, but there are plenty of streaks that went on even longer.

My goal on a ski vacation is to have fun. I think that’s mostly about some sick pow, big laughs, and fast friends. But I can’t let the mix of returns impact the ultimate goal. Some of my vertical came from whiskey flights and not mountain tops, and that’s okay. The fancy new lodge I groaned about happens to have an exceptional ski school. I’m guaranteed to get it wrong if I’m trying to be smarter than the market or time the weather.

Why be bitter that your long term return came from bubbles followed by crashes if you either a) never touched your assets or b) structured your portfolio to be robust against this volatility.

While he gained notoriety from the comment’s subprime context just months before the CDO explosion, I find the quip from then CEO of Citigroup Chuck Prince apropos. “When the music stops, in terms of liquidity, things will be complicated. But as long as the music is playing, you’ve got to get up and dance. We’re still dancing.”

You shouldn’t let your portfolio get Citigroup complicated. But with a reasonable plan for the exits, you’ve also got to dance to whatever music is playing. The market delivers on its preference, not yours. Tips forward, enjoy whatever bumps you hit.