When she moves, she moves

Vol #39 - May 21, 2021

It’s the stage in the bull market where I start quoting Ricky Martin.

“Oh baby when she moves, she moves

I go crazy 'cause she looks like a flower

But she stings like a bee”

When the market moves, it moves, and it can really sting like a bee.

We’ve seen a relatively significant deleveraging amongst risk assets this week. Bitcoin has been falling like a stone. Broad equity indices have also been exhibiting choppiness. Last week we saw a lurch and rebound, and this week is playing out similarly.

For nearly two months investors had been lulled into the complacency that comes with repeated all time highs. Implied volatility as measured by the VIX index never crossed 20 during the month of April. With little movement at a macro level, the fear index settled into a tight range around 17%. That level of implied volatility means the underlying is expected to move around at a little over 1% a day.

From the beginning of April until last week, the average daily move in the SPX was less than half a percent. Only three of those 25 market days saw movement of more than 1% - all to the upside. The following 10 days had 4 moves greater than 1%.

The story for Bitcoin is even starker. During that same time period, implied volatility was relatively low - averaging about 70%. That implies daily moves of a little over 4.3%. The average actual move was only about 2.7%. While not exactly at the all time highs, the digital asset came into May up 87% on the year.

But as we see time and again, markets rarely behave in a nice uniform fashion. Most days the markets are going to move less than the implied volatility suggests. There’s always a degree of extreme risk priced into these insurance contracts.

Options don’t price volatility for the average day, they have to price it for the abnormal day. There must be enough risk premium included to account for what happens when markets really shift.

Another part of this is pricing economics. If you’re always selling insurance (writing options) at exactly your loss ratio, there’s no profit margin. Writers of options typically expect to earn some variance risk premium in return for providing risk capital to buyers in the marketplace.

Fundamentally we expect these moves to happen. Volatility is the price we pay for earning excess returns. But they always seem to happen all at once.

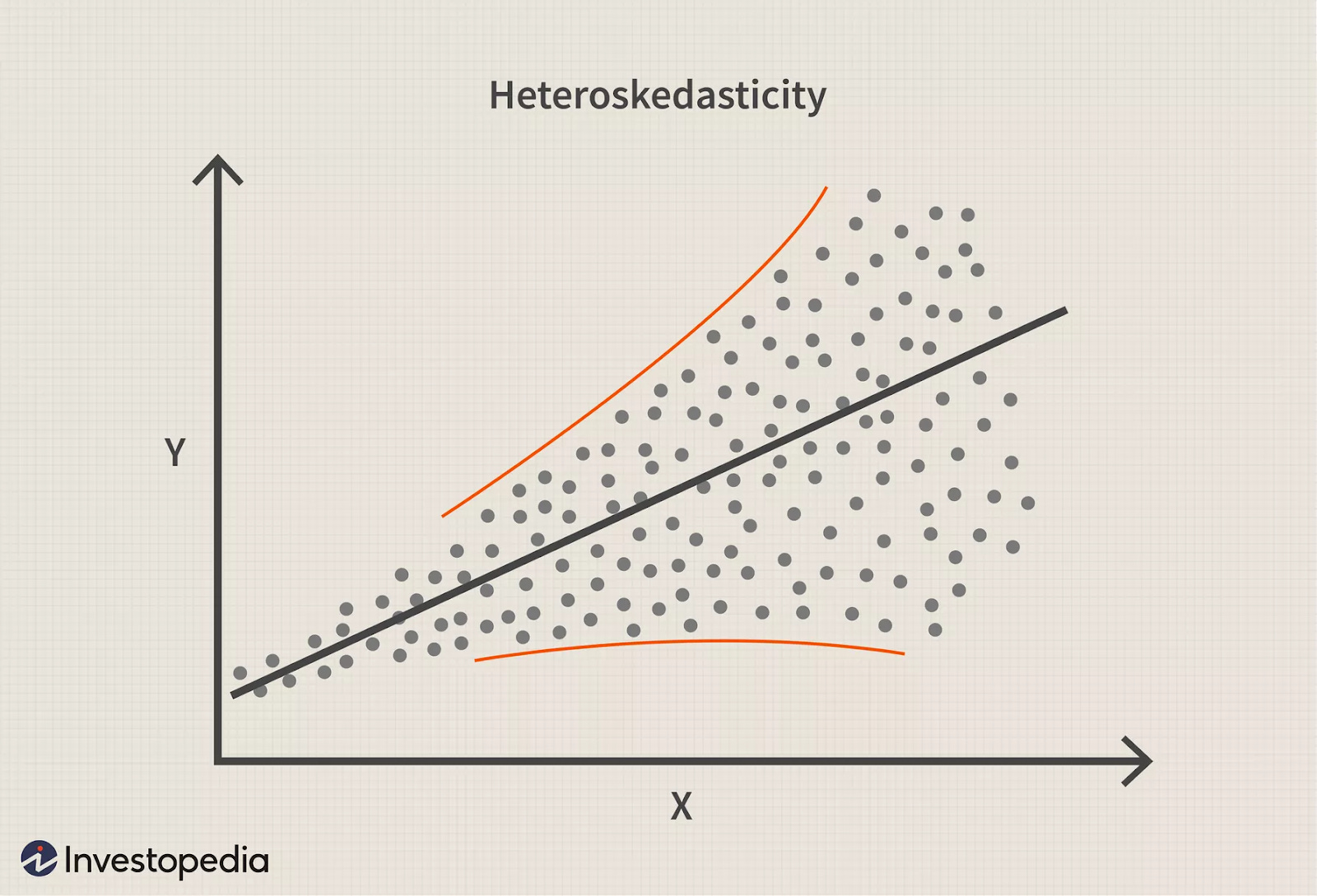

There’s a statistical concept that applies very well to market dynamics - heteroskedasticity. Technically speaking, this occurs when “the standard deviations of a predicted variable, monitored over different values of an independent variable or as related to prior time periods, are non-constant.”

Just like Ricky Martin said - when she moves, she moves.

Markets can be very calm for long stretches of time, and then burst out of their coil. This doesn’t mean that after a long period of low volatility, the probability of something happening increases - that’s akin to the Gambler’s Fallacy.

What heteroskedasticity suggests, is that when you have high volatility one day, it is likely to beget high volatility the next day. Volatility clusters. Regimes shift. Not only do prices ebb and flow, the rate at which they change ebbs and flows.

Heteroskedasticity describes the phenomenon, but it doesn’t completely answer the question of why.

At the end of the day, market participants are human. News percolates out not in a steady stream but in fits and starts. The narrative swirls. Observed price action has a reflexive effect on participants. There’s a big difference between seeing a 2% or 20% drop in a spreadsheet and actually being able to hold on to your position.

Another part of that is the current environment where the prices of risk assets have ballooned in a system awash with cheap money. There are real dollars being helicoptered into bank accounts, and paper millionaires being minted every minute in a merry go round of euphoria.

The more hot money is flowing through a system, the faster things are going to move. De-risking is a cross asset activity, such that a sneeze in one community can spread contagion across markets.

Risk capital is able to move between speculative assets faster than ever. It only takes a few clicks on your phone to turn dollars into stocks, coins, or tokens and then back again. This in turn drives the velocity of price in these same assets.

The markets are bursting with opportunities, and volatility of price action is part of that. But change is always just around the corner, and investors have to be prepared not just for the merry go round to stop, but for it to speed up or slow down.