When the Time is Right

Vol #186: July 18th, 2024

The neighbors caught us red handed. Juice spattered hands and a bowl full of raspberries.

While they would soon become our friends, it was awkward being found harvesting their once a summer fruit. The bushes were on the road side of the fence, but distinctly their property.

For several years my sister and I walked the three tenths of a mile over to our neighborhood bramble. Poking our tiny hands between the thorns, we would collect a pint to bring home and eat twice as much along the way.

The new family was accommodating to thieves. It was raspberry season. Wild berries come sometime in July when the flesh is as delicate as the bushes are prickly.

This week I continued that tradition, and took my berry hunting chihuahua and daughter out collecting. Our yard is full of them. No adult, canine, or juvenile delinquency required.

If you come over for dinner this week, guess what’s on the menu. Muddled with mint and mezcal. A savory gastrique for the salmon. Wild raspberry ice cream. ‘Tis the season; get ‘em while they’re fresh. I don’t have my grandmother’s patience to jam these, so we enjoy them today.

The calendar moves ceaselessly forward. If you want a red fruit tart, don’t come knocking in November. If you want to trade a multi-legged strategy in equity options, stay away from the sixth weekly expiration.

A good options strategy aligns both with a theoretical target, and the realities of market structure. Liquidity and strike selection might not always line up with round numbers, but it is fairly predictable.

Structure and participation determine liquidity. You need tradeable contracts with appropriate strike listings and expirations, but also traders and dealers deploying their resources. Granularity is a balance. Fragmented capital creates wider markets, but more customizability encourages customers and their coveted orderflow.

There are currently 361 unique price levels across all expirations in SPY. That’s up from an average of 275 only five years ago. Spread across expirations, that makes for 4903 combinations of time and price. That count is up almost 60% in the same period. Weeklies, dollar strikes, end of month, quarter, etc. For top tier issues, there’s almost always a strike in range.

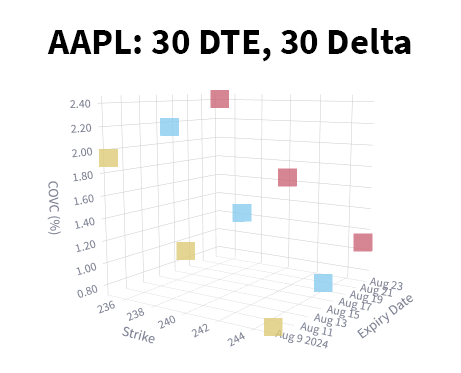

Strikes are denominated in dollars, but $5 apart is a gaping hole in a $225, 31% vol stock, and peanuts in a $3000 31% vol stock. It would be silly to list $1 strikes in $BKNG, but I distinctly wish $AAPL had something better than $5 apart in Aug - that’s only 30 days out. There’s a pretty big variation in the premium collection for these targets around 30 DTE, 30 Delta calls.

Delta is a good way to normalize things in the options world. It wrangles percentages and implied volatilities to make for easy comparisons. I like to use delta targets in strategy design as it remains a consistent barometer across market environments.

We can also use this metric to measure the quality of strike listings. For any given delta, how close are my strike choices? Liquidity is about width and volume, but the selections on the menu also matter quite a bit.

A new metric that I’ve developed is called “StrikeScore”, and it’s the number of deltas away a strike is for any given expiration or issue. If you’re targeting the 30 delta call, and the nearest $240 strike is 35.2 delta, that’s 5.2 deltas away. Averaging this across all target deltas from 1-99, we get a score.

It’s no surprise that SPX tops the list here. Across all the expirations, on average there is a strike within a half of a delta (.46) of any given target. I don’t know many - if any - strategies that require that level of precision.

SPX has liquidity going for it - that’s a given. But another major factor is the price level. In terms of absolute averages, META, COST are up in the top ten, and are both reasonably liquid issues. But so are IVV, FICO and BKNG. Those aren’t even Top250 issues, but they score very well because $1 and $5 intervals finely slice a $556/$1604/$3990 stock.

There is a two sided dynamic to having more expirations. Sometimes additional terms boost the score by the added precision of more strikes in the very short term, other times the first weekly to roll on only has a handful of strikes far apart and punishes the rank.

Another part of it is how the rubber hits the road with break points and listings choices. At certain dollar amounts the intervals change. Where this hits the implied volatility curve might create more choppiness in delta.

While these micro-structure nuances matter at the margin, a predictable place to get better strike listings is in serial expirations. In the case of SPX these will have been listed for at least a year, and at least 3-6 months for other names. Open interest has time to accrue which gets more people interested in trading, and there is often a greater range of price levels touched, resulting in a wider range of strikes.

If we only look at the score for months that are serial expirations, SPY drops to a .46 reading, and SPX gets even tighter at .38. QQQ also jumps back onto the podium at .65. Killer readings for the indices.

Across all of the Top250 issues, the average difference is 3 deltas. 3 deltas is not a lot. Trade any of these names, and there’s likely to be a pretty good strike. Even if you broaden your filter 10x, and take every name that trades more than 100 contracts a day, you’re only 6 deltas away.

Good strikes don’t always mean good markets unfortunately. Liquidity is well measured by spread width, and we have gaping chasms for 90% of the options listed. It’s even dicey at the 95th percentile (roughly issue #250). But they’re there, and that’s a good start.

For the names worth trafficking in, both liquidity and strike count are better in the expirations that have been listed for longer periods of time. It’s not going to double your PnL, but this trend is both as material and consistent as VRP.

There are lots of factors that go into choosing the trade parameters. End of month options exist because they line up with accounting periods. For defined outcome “boomer candy” ETF products, FLEX options are used for strike precision.

Trading the most liquid market should rank high in your selection criteria. All other things being equal, the serial expirations have the most favorable conditions. The chance of another side price improving, or the strike hitting right at your premium level is just a little bit better.

Sure there's a 14 DTE Thursday options contract listed. The grocery store has raspberries all summer long. But if you’re only gonna make gastrique once - do it when the time is right.

Interested in reading more about StrikeScore?

Tomorrow’s edition of Portfolio Design will dig into trends over time, the relationship with volume, and what this means for strategy implementation.