The cheeseburger sub is a glorious invention.

I personally discovered this at a local Italian joint in Medford MA. I wasn’t exactly a take-out aficionado heading into college, but I’d certainly never seen anything like this. Steak and cheese calzone, wait your turn.

There are few things harder to pin down than where a food or beverage was invented. It’s obvious why record keeping about the first Manhattan is fuzzy. There’s a rough story about a sixteen year old kid in Pasadena putting cheese on ground beef, and the best we can do about the grinder/hoagie/wedge is peg “submarine” to the general area in Groton CT where these torpedoes were built.

So good luck finding where this mule of a dish came from. More than just a bun shift, the hero version of an American classic splits the patties and lines these glistening Maillard half moons over a bed of lettuce, tomato, pickles, and onions.

Many great dishes are robust to experimentation. The dumpling has found its way into nearly every global culture. But that’s not true for everything. Twenty first century logistics can deliver fresh PEI oysters around the continent, yet we haven’t quite solved the grocery store sushi problem.

Some things are not meant to be packaged. I don’t need Jiro slicing the toro in front of me; but once you put fish under a clamshell wrapper you’ve killed the spirit. It’s not just the lost texture of freshness and dichotomy of warm rice vs. chilled meat- you’re getting a lower quality product. Soggy nori wraps pair wonderfully with yesterday’s catch.

The ETF industrial complex is built on processing and packaging securities. The brilliance of the structure is that it provides a one click, instantly tradable vehicle with exposure to an underlying strategy. It also gets some clever tax treatment as securities are rotated in and out.

Most investors know that there’s more to do than just buy a stock and come back in thirty years. Winners must be sold as they fade, and laggards dropped. Diversification prevents concentration risk, and the friendly advisors and fund administrators will do all this for an annual fee of well less than 1%. Because the scale and competition has exploded, many places will do it for less than 10 bps.

While I certainly could, I don’t make my own yogurt or bake my own bread. Upon discovering that most vanilla extract sits around for 12-18 months to develop its flavor, I now happily pay the Madagascar rates. It wouldn’t be cost or time effective for me to rebalance my broad US equities exposure either. ETFs of any reasonable flavor are ubiquitous, and they do it well.

In fact the funds have gotten so good - perhaps even better with Target Date implementations - that the packaged off the shelf product is better than any home cooking. It would take significant scale and a suspiciously high level of expertise for the home grown version to do a better job.

But let’s not confuse the efficacy in one domain for another. Options strategies don’t belong in an ETF wrapper. It’s worse than just paying for your broker’s yacht - you’re also punching holes in your own water craft. The marriage of these two strategies is an abomination to both of their lineages.

I love covered calls. They’re the most obvious entry point for equity options strategies. There’s the VRP benefit of collecting short volatility premium and remaining long the underlying. Stock analysis is also something familiar to investors. If you work with the right underlyings and use discretion on timing, it’s a strategy that enhances the return profile and makes you money.

Given the intuition of this trade, options funds have run with it. When the trade structure gets interpreted by snake oil marketers, the cash flows and benefits of the strategy sound like a golden goose. Income? Equity? Risk Management? Cha-ching.

The problem is a systematic options strategy that does only one thing is none of those. It’s a wealth destroying vehicle for everyone but the managers. ETF option manufacturing plants would make Upton Sinclair nauseous. The packaging is as naive as it is malicious. I’ll take the Stop&Shop hamachi instead.

What makes an ETF work with equities is not what works with options. Systematically diversifying your stock exposure has a long proven track record. Being able to hold many assets for small dollar amounts is a true democratization. Slinging calls and calling it income not so much. Stocks get better when you package them - options strategies don’t.

The most important feature of an option is its expiration date. While you might be tempted to say volatility, that number only matters because you cap the holding period. This necessitates turnover and rebalancing. Where rebalancing is a positive opportunity for equity baskets, it’s more complicated with a covered call.

Just as equities may be under or overpriced, so are options. In the long run, particularly in the most liquid products, implied volatility is well priced. This is a good reason to feel comfortable trading with current pricing, but it’s not a good reason to always apply the same axe.

When it comes time for QQQ to look at its future quarterly composition, it is naturally trend following - buying more of the leaders (those that have increased in market cap) and selling the laggards. Rebalancing is an edge.

Not true of a covered call strategy. If your mandate is to sell the TSLA covered call for income, you’re going to sell the call whether the price is right or not. It’s a crapshoot based on where the sun, moon, and the VIX are.

Things get even worse if you’re targeting cash levels. Low volatility will cause you to sell increasingly higher delta options to achieve that same dollar amount, altering the return profile. No matter which way the stock goes, TSLA calls are not always a sale.

But the worst part about the day old bottom feeders, hemmed in by little plastic fences, basking in fluorescent light? They don’t even taste good. They underperform.

To pick on one - this was easy, there are many - the TSLY product writes options on TSLA to generate a 115% distribution rate. Last month they paid $1.09, so yes that arithmetic works for a $12.35 stock, but it’s still nonsense.

Over the last year, distributions included, TSLY (bars) is down almost 13% while TSLA (purple line) is down just over 7%. There are periods where you see the covered call fund outperform, but it’s never enough to outpace the upside. Some of that is natural for covered calls, you are giving away the right tail.

TSLA is a decent benchmark for the TSLY overwrite, but a better one would be other overwrites. Without a single attempt at datamining, my first two “go-to” strategies for TSLA overwrites outperformed this.

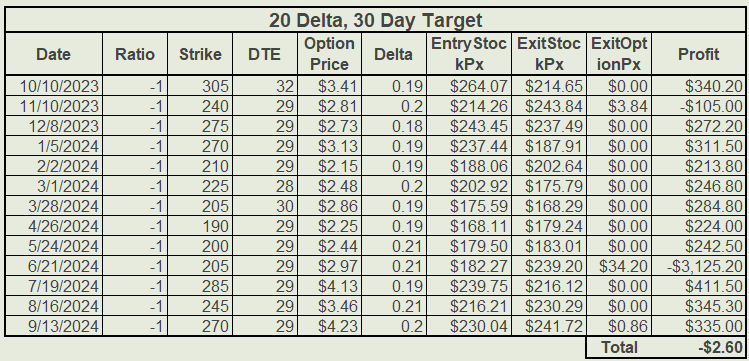

Targeting a monthly distribution, we start by writing monthly covered calls. Even if we want to go so far as always selling, I think it’s extremely prudent to use delta. At least that adjusts relative level to the volatility environment. Targeting the 20 delta level yields an options PnL of -$2.50, while the 30 delta level is a profit of $380. Trade details here1.

While neither of these are alpha nuggets, even a naive implementation of the covered call strategy doesn’t drag 5 additional percentage points worse than the underlying. You’re basically in line.

Just as I say that covered calls aren’t always a sale, the argument by these funds will be that they are not evergreen strategies, and they’re designed to be traded and allocated.

That works for many structured ETFs. The VXX product is not a great way to be long vol for the duration, but as a short term proxy for daily volatility moves it does a good job. The same thing is true for leveraged long and short products. But if you’re going through the effort of timing, why aren’t you just trading/not trading the overwrite itself?

Income generation ETFs are fueling demand for a strategy that is fundamentally broken and intentionally misrepresented. These strategies want to look like a portfolio allocation. They steal the valor of option’s hallmark strategy. Masquerading as an investment product, the disclaimers show they’re just a fee engine which converts your (reduced) cash into a tax liability.

Holding the underlying equity throughout the year has no tax implications. Trading your covered calls yourself would leave you with small short term gains/losses. TLSY however, has paid out $9.84 or 41% of its $24 starting value in distributions. Your position is down 13% AND you have to pay the dividend tax rate on almost half of it.

Even if you’re trading with an IRA or focused on a distribution scenario - why wouldn’t you just buy t-bills and sell off what you need?

When making investment decisions, it’s important to know what types of products fit where. There’s plenty of good stuff in the frozen food section, but souffle isn’t going to be one of them. Take advantage of the glorious efficiency of an ETF for indices, sectors, and exposure to things like GLD.

Just please make sure your options are over them, not in them.