No Size Fits All

Vol #62 - December 3, 2021

If you’re sweating, it’s time to turn down the heat.

Equity markets saw a series of fits and starts this week, with the standard cocktail of sell offs chased with buy the dip, and a dash of intra-day turnaround.

The recipe is tried and true - volatility begets volatility. Ricky Martin and I agree; When she moves she moves.

If you’re worried about risk management on a week like this, you’re running too hot. Variance like this is not only expected, it’s a healthy steam valve and creator of opportunity.

Whether managing a professional book or your own portfolio, building in allowances for this kind of variance are important on the offensive and defensive side of the house. It’s going to happen, so you better have a plan and make sure you’re sized accordingly.

Financial market volatility demonstrates heteroskedasticity - the clustering of variance. If the options market pricing predicts that the broad market will move 1% a day on average, not only does that daily figure vary, but how much it varies follows a second order pattern.

When one day the market moves by 3%, the next day is more likely to be an outsized move than a reversion to the mean of 1%. Like a fever, this string of high vol days abates and over the medium and long run the variance falls back towards long term levels.

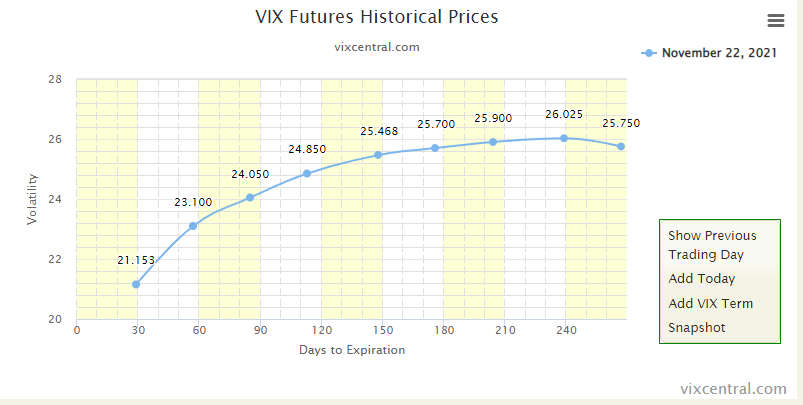

To put this week’s (relatively minor) turbulence in perspective, we can look at the term structure of VIX futures. A quick way to think about this is, how much do investors think the market will be moving at different time periods in the future. For the medium term, 6 month to 2 year time frame, the curve is flat between 25 - 26.

The VIX index itself was around 18 at the time of this snapshot. This week we saw it “spike” as high as 31. Those numbers are pretty consistent with medium term volatility forecasts in the marketplace.

Proactively, the best way to manage risk is through position sizing. Everything comes back to how big you put on the trade. Your entire PnL is a conviction multiplier of your size.

When you enter into a position, there should always be a game plan for how to manage what can happen. If you’re investing for the long term, close your eyes and dollar cost average are the best pieces of advice. When you have shorter horizons, setting investment and divestment levels ex-ante binds you to an Odyssian contract and reduces the emotional element.

When managing a more dynamic portfolio, your position sizing should be a function of the multiple dimensions of risk management. Each strategy and investor must evaluate what their capacity, tolerance, and appetite for risk are.

Capacity is your ability to economically withstand the variance of your strategy. No matter how badly I may have wanted to break the Bank of England, George Soros was in a much better position to put on the trade than me.

A good risk management protocol maximizes your capacity. Poker watchers like to romanticize going “all in”, but this is a foolish way to manage money. The size of your trade should be designed to optimize your edge capture over repeated at-bats. The more times you can step to the plate with positive expectancy, the lower your PnL variance and greater compounding.

Risk tolerance is the emotional dimension of the position sizing.

You should never let a position keep you up at night. Being short gamma (you lose when things move) can be difficult for many traders because of the patience and mental fortitude required to extract payment.

If the position size is misaligned with the risk tolerance, an investor is more likely to make snap decisions based on price action. The best strategy and size for an investor is the one that doesn’t impact the rest of their life.

Finally there must be an appetite for risk. Even with the capacity and tolerance for large size, it should not come automatically. Without interest or desire, risk acceptant investments will always disappoint.

How to size your position is the most important decision you’ll make in investing. It depends on your strategy, personality, and bankroll. While there’s no textbook answer, for any strategy to have durability, it must expect and be robust to variance.