So You're Telling Me There's a Chance

Vol #59 - November 5th, 2021

Standing atop a mountain, skiers will map out their line and then “drop in”.

The steepest part of the hill is usually right at the top. While there are ups and downs, and changes of slope along the way (that’s what makes it interesting!) generally things flatten out as you approach the bottom.

When trading options and waiting until expiration, “drop out” is probably a better way to describe the experience. An options value stays fairly consistent throughout its life, until the final days and hours when things start moving fast.

We can break down an option's value into two distinct components. The intrinsic value is what that option would be worth if everything stopped right now. If you own the $140 strike call - the right to purchase stock - and the equity is trading $150, that’s worth at least $10. Exercise the call to buy stock for $140, sell the stock at $150, $10 of value.

The extrinsic value is where things get interesting. This is all the je-ne-sais-quoi of time and volatility and future expectations distilled down into a premium over intrinsic value. Everything that makes an option feel like a lottery ticket is extrinsic value.

Last week we talked about how high volatility and a long time frame opens up a lot of different potential price paths and how the options pricing model needs to account for them. This makes intuitive sense - lots of time, lots of possibilities.

How do we account for the changing landscape of possibilities? What is the impact of each passing hour on the clock?

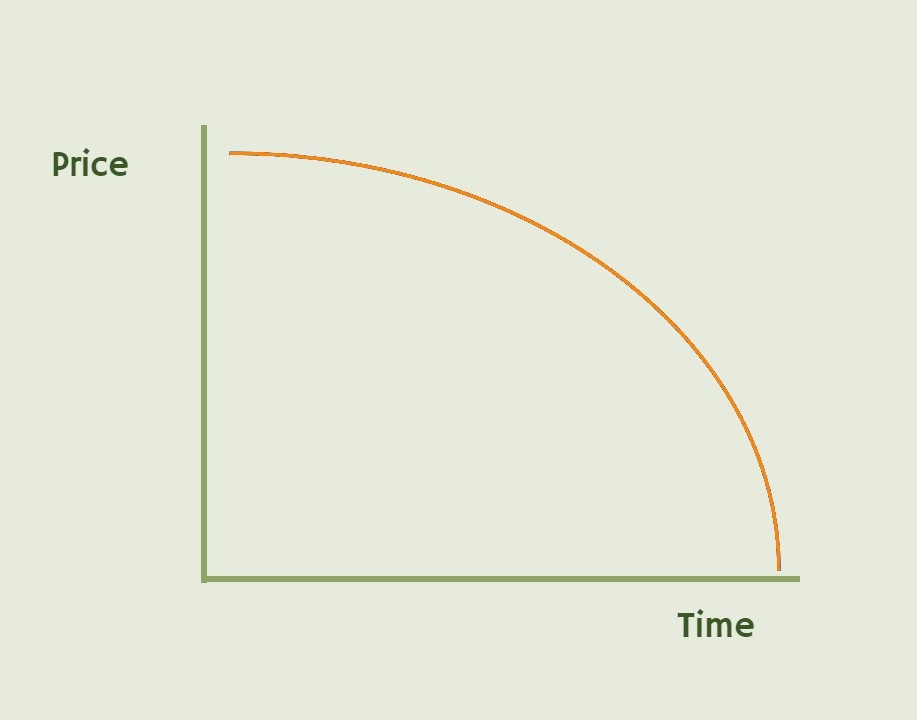

The rate at which an options price changes with respect to time passing is called theta. If nothing else changes, and we get one day closer to expiration, the amount of extrinsic value that an option loses with a little less time left is theta decay.

What’s less intuitive is how this extrinsic value should change over time. With options pricing questions I always like to start with the extremes. If you have an option that is struck 1 year out in the future and a single day passes, you’d expect very little to change. But if it goes from 1 day to 0 days, everything changes.

In markets - as in life - anything can happen if there’s still time on the clock. Sports fans know this viscerally, hanging on threads of hope for buzzer beating shots.

Theta decay is not linear. Early in an options life the curve looks very flat. Each passing day a little bit goes away, and one day looks like the next - there’s still plenty of time left!

As things get close to expiration, the pace quickens, and small movements have a big effect. When stock moves a few dollars and there’s still 6 months on the clock, it barely has an impact. But a few dollars move with a few hours left completely changes the payoffs of near the money options.

The steepest part of the curve is at the end. The bottom drops out. Long option holders know this because they wait patiently for their expected movement to happen, seeing their account value slowly dribble down until - poof - it’s all gone at expiration.

On the short side, sellers of options must be very patient. Writing that insurance awards them premium potential, but the majority of it doesn’t come until the final day. One can’t close the door on possibilities until the very end.

This effect is exaggerated by volatility. When something is highly volatile, those final minutes still include a wide range of price paths, and options pricing must account for that. If Michael Jordan still has time on the court, you don’t leave the United Center.

Knowing how to manage your decay is important for any options strategy. There are ways to win on the short side, and ways to win on the long side, but too much of either can leave you exposed to last minute surprises.